General Mills, Inc. (NYSE: GIS) released its fiscal second quarter 2026 earnings on December 17, 2025, once again placing one of America’s oldest and most iconic consumer staples companies under the microscope of investors and industry analysts. Known as the maker of Cheerios, Pillsbury, Betty Crocker, Blue Buffalo, and Häagen-Dazs, General Mills’ performance reflects the complex interplay between consumer behaviour, pricing strategies, global supply chain pressures, and transformational initiatives. As part of this detailed analysis, we will unpack the latest GIS Financial Report data, interpret its deeper meanings, evaluate strategic drivers for future growth, and ultimately assess the implications for GIS stock price and investor positioning. This article integrates broader industry dynamics while providing specific data-based insights into business performance, future prospects, and long-term valuation.

1. Summary of Q2 Fiscal 2026 Results: Top-Line and Bottom-Line Overview

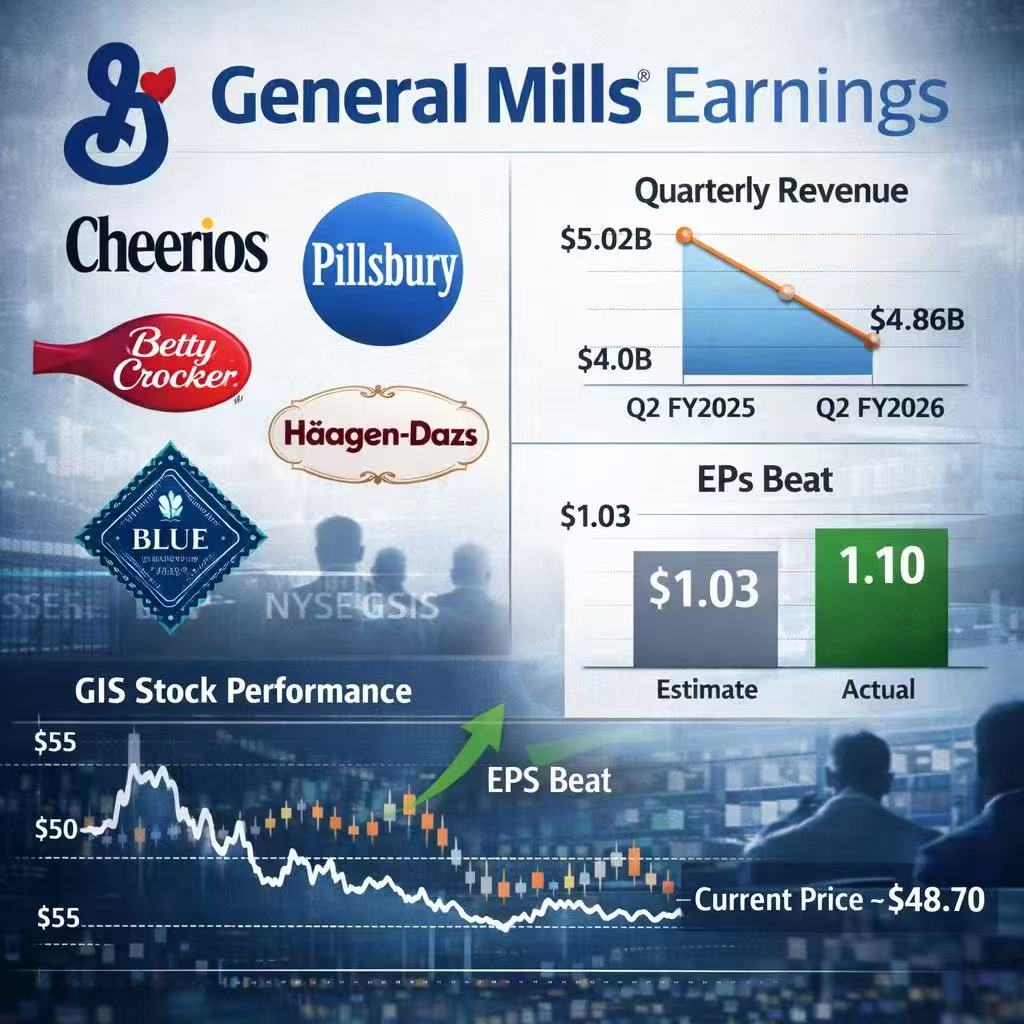

In its December 17 2025 earnings release, General Mills reported quarterly revenue of approximately $4.86 billion, slightly surpassing consensus expectations of roughly $4.78 billion. Net sales for the period were down year-over-year by approximately 7% — a decline largely attributable to the divestiture of its U.S. yogurt business (including popular brands like Yoplait and Go-Gurt), which exerted close to a 6% headwind on reported sales figures. Despite the decline in net sales, the company delivered an adjusted earnings per share (EPS) of $1.10, beating analysts’ projections near $1.02–$1.03 and outperforming most forecast models. This combination of weaker top-line performance and stronger-than-expected bottom-line results underscores a mixed but ultimately resilient earnings pattern for General Mills.

While revenue contraction reflects ongoing market pressures, the ability to beat on EPS demonstrates strong cost discipline and margin focus. For context, General Mills reported comparable EPS and revenue beats in prior quarters, indicating a continued trend of executive management effectively navigating macroeconomic headwinds.

2. Revenue Breakdown: Disentangling Organic Growth and Structural Changes

To fully understand the revenue trends in the latest General Mills Earnings release, it is critical to separate underlying organic sales performance from structural accounting effects like divestitures.

2.1 Organic Net Sales vs Divestiture Impact

Organic net sales — which reflect pure underlying business activity excluding portfolio changes — were relatively modest, with some segments showing slight growth while others reported declines. The U.S. market, traditionally the largest contributor to General Mills’ revenue (often exceeding 80% of the total), displayed slower consumer demand in select categories like packaged snacks and certain cereal segments, driven by both inflationary pressures and shifting consumer preferences toward healthier or private-label alternatives.

At the same time, divestitures such as the sale of the yogurt portfolio materially lowered total reported revenue figures. The yogurt business historically accounted for mid-single-digit percentage points of revenue contribution, meaning that without this structural change, reported net sales might have shown a less severe decline. Factoring out divestitures, organic declines in key categories appear to be closer to mid-single digits rather than sharp contractions, a nuance important for investors interpreting the latest GIS Financial Report.

2.2 Segment-Level Performance

Across business segments, performance was uneven:

- North America Retail faced significant headwinds, with volume pressure and a reduction in price/mix effects continuing to weigh on total retail sales. Price resets and promotional spending intended to support volume recovery further compressed reported revenue figures.

- Pet Products, led by the Blue Buffalo brand, remained a comparatively resilient growth engine, offsetting some weakness in traditional grocery categories; however, marketing and launch investments in fresh pet food products temporarily weighed on margins.

- International Revenue growth remained mild but positive in select regions, suggesting that geographic diversification, while modest in size, is contributing incremental performance outside the core U.S. market.

Overall, the revenue mix reflects a business undergoing structural transition — where short-term sales declines are juxtaposed with strategic investments and transformations.

3. Profitability and Margin Dynamics: EPS Beat in Context

General Mills’ adjusted EPS of $1.10 represented outperformance relative to the consensus — a signal that cost controls and operational efficiencies are delivering measurable results. This beat underscores the company’s ability to navigate inflationary input costs, logistics disruptions, and promotional pressures.

3.1 Gross Margin Pressures

Despite the EPS beat, gross margins faced some headwinds due to:

- Higher input costs driven by ongoing commodity pricing volatility

- Promotional price investments aimed at stimulating volume demand

- Tariff-related effects on international goods movement

These factors collectively squeezed pricing power and margins, especially in North America Retail segments where pricing resets were more pronounced. Margin compression was partially offset by supply chain efficiencies and cost-of-goods-sold optimizations implemented in prior quarters.

3.2 Operating Expense Management

Operating expenses were managed with discipline, and while marketing and innovation spending increased, the company made targeted investments in areas expected to yield future growth rather than broad-based administrative expansion. This allocation strategy aligns with long-term brand positioning and reflects management’s emphasis on sustainable profitability rather than short-term cost reduction.

4. Strategic Initiatives and Innovation: Beyond the Numbers

One of the key takeaways from the latest GIS Financial Report is that much of the company’s strategic focus is not fully captured within headline revenue or EPS figures. Rather, long-range pivot efforts are underway that stand to influence future earnings growth and business resilience.

4.1 Brand Innovation and Health-Conscious Consumer Trends

General Mills continues to innovate across its product portfolio, particularly within premium, health-conscious, and plant-based segments. Investments like removing synthetic dyes from its retail products over time and the expansion of organic or minimally processed offerings align with broader consumer trends toward healthier eating habits. These efforts, while potentially compressing near-term margins, are designed to bolster long-term demand and differentiate brands in competitive markets.

4.2 Pet Food Expansion: A Strategic Growth Lever

The pet segment, especially within premium cat and dog food, represents one of the more dynamic growth areas for General Mills. Blue Buffalo, one of the company’s marquee pet brands, continues to capture share in a market less susceptible to the volatility impacting traditional grocery categories. Investments in fresh pet food initiatives are intended to capture incremental consumer expenditure, though they also bring higher marketing and launch costs before meaningful revenue turnover materializes.

4.3 International and Channel Expansion

General Mills’ international footprint plays a secondary but strategic role in the company’s growth roadmap. Markets in Latin America, Asia, and Europe present opportunities for portfolio expansion, brand licensing, and channel diversification. While these markets typically represent a smaller share of total revenue compared to the U.S., positive trends in certain regional segments suggest that international contributions could improve future top-line performance.

5. Comprehensive Risk Assessment: Headwinds and Vulnerabilities

While the latest earnings provide pockets of resilience, multiple risk factors remain integral to any assessment of General Mills stock:

- Persistent volume pressure — particularly in legacy grocery categories

- Margin compression due to promotional pricing and cost pressures

- Evolution of consumer preferences toward healthier or private-label alternatives

- Commodity cost volatility impacting gross margins unpredictably

Additionally, historical patterns indicate that GIS stock often trades lower in the immediate aftermath of earnings announcements, reflecting investor caution and skepticism in a low-growth environment.

Despite these challenges, the company’s strong dividend yield and brand portfolio provide a defensive buffer in a turbulent consumer landscape.

6. Market Reaction: GIS Stock Price in Context

As of December 18, 2025, General Mills’ shares are trading near $48.70, showing modest volatility but maintaining a stable valuation within the broader consumer staples sector. The GIS stock price reflects both the defensive nature of the business and investor uncertainty over sustained growth. It trades at valuation multiples that imply tempered expectations compared to high-growth sectors but remains attractive relative to many defensive peers.

Dividend investors especially note the company’s attractive yield, which enhances total return prospects even in periods of flat share price movement.

7. GIS Financial Report Outlook: What Comes Next?

Looking forward, the trajectory of General Mills’ performance will likely hinge upon:

- Execution of volume recovery strategies, especially in core retail categories

- Conversion of pet food investments into profitable revenue streams

- Expansion of international footprint and strategic product innovations

- Margin management in the face of inflationary and commodity pressures

Guidance for fiscal 2026 suggests organic net sales may fluctuate modestly (between slight growth and slight contraction), but overall profitability remains stable based on current market assumptions.

8. Investment Recommendation: Buy, Hold, or Sell GIS Stock?

Based on the comprehensive analysis above, the current earnings performance and future outlook point toward a Hold recommendation:

Why Hold?

- The company delivers consistent earnings beats even amid revenue challenges

- Defensive brand portfolio and reliable dividend yield support stable returns

- Long-term strategic initiatives enhance future growth potential

Why Not Buy Aggressively Now?

- Top-line contraction persists in core markets

- Growth catalysts are longer-term and not immediately accretive

- Investor sentiment remains cautious until volume recovery materializes

Sell Only If:

- Macro pressures accelerate faster than expected

- Volume declines deepen beyond current projections

- Dividend prospects are materially impacted by margin erosion

Overall, Hold captures the balanced nature of the company’s near-term risk/reward profile.

Conclusion: A Mature Business Navigating Transition

The December 17 earnings release highlights General Mills’ ability to outperform expectations while managing structural shifts within its business. The latest GIS Financial Report lays bare the inherent tension between short-term sales declines and long-term strategic investments. For investors considering General Mills stock, the narrative is one of resilience rather than rapid expansion — a characteristic consistent with defensive stocks in the consumer staples sector.

As the business navigates changes in consumer behaviour, cost pressures, and category evolution, it remains a key benchmark for defensive staples performance, supported by strong brand equity and disciplined financial management.

Leave a Reply