After a four-month sell-off, the market’s enthusiasm for Palantir has been reignited by the growth potential of its defense business, with Wall Street’s bullish sentiment approaching historical highs.

After a four-month sell-off, the growth potential of Palantir’s defense business has reignited the market’s enthusiasm, and Wall Street’s bullish sentiment on the stock is nearing historical highs.

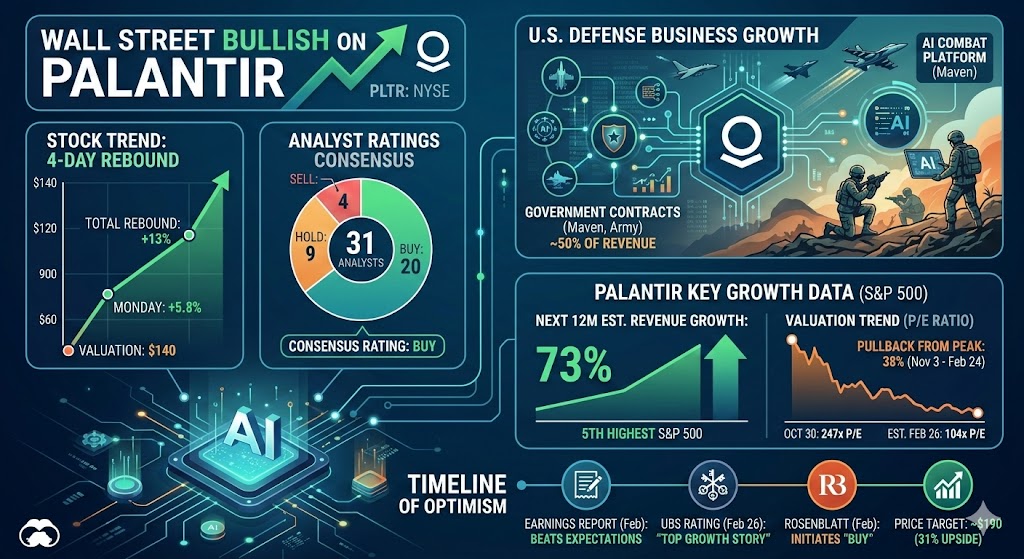

The data analytics software company derives about half of its revenue from U.S. government and military contracts. As President Trump escalates threats against Iran and the U.S. and Israel launch military strikes against the country, the stock has been rebounding since last week, with a 5.8% rise on Monday and a total gain of 13% over four trading days. The Trump administration anticipates the conflict may last for several weeks, while Iranian officials suggest it could extend longer.

“The stock price rise is an emotional response to Palantir’s strategic position within the government and military,” said Tim Paliara, Chief Investment Officer at Capwealth Advisors, which holds shares in the company. “I don’t think the war will significantly change Palantir’s fundamentals, but it validates Palantir’s standing within the government, laying the foundation for its continued growth and penetration in various military sectors. This conflict precisely underscores the company’s deep embedding in the government system and its moat.”

Palantir, long criticized by analysts for its high valuation, underwent a substantial pullback last month, falling 38% from its historical high on November 3 to a low on February 24. During this period, investor Michael Burry, famous for his role in The Big Short, launched a strong criticism of the stock, mainly concerned about its valuation and growth potential, as well as its ties with U.S. Immigration and Customs Enforcement (ICE) and the Department of Homeland Security (DHS).

As a long-time U.S. government contractor, Palantir primarily works with the military and ICE. In 2024, the company secured a $100 million contract to provide an AI combat management platform, the Maven intelligent system, for integrated military data. Last summer, the U.S. Army awarded Palantir a $10 billion contract, with the government stating that it would shorten procurement cycles to “ensure soldiers quickly gain access to cutting-edge data integration, analysis, and AI tools.”

Even before the escalation of the Iran conflict, Wall Street analysts had turned optimistic on Palantir. While concerns about AI disruption in the software industry partly explain the pullback from its peak, the market generally views Palantir as a beneficiary of AI, and the company’s strong earnings report has validated this view.

“Palantir has demonstrated a sustainable growth path in a challenging environment,” said Dave Mazza, CEO of Roundhill Investments, whose Roundhill Generative AI & Technology ETF holds shares in the company. “Analysts upgrading their ratings indicate that the fundamentals are quite strong.”

However, risks remain due to the high valuation. Palantir is one of the most expensive stocks in the S&P 500, with a projected price-to-earnings (P/E) ratio of about 104x for the next 12 months, and a price-to-sales (P/S) ratio of 45x, the highest among S&P 500 constituents. Of course, this has significantly decreased from the 247x P/E ratio and 89x P/S ratio projected on October 30, making the current stock price appear relatively cheaper.

“If analysts were bullish on its fundamentals at $200, they’re even more bullish at $140,” Mazza said.

Analysts have raised their ratings, with Rosenblatt Securities initiating coverage with a “Buy” rating, significantly boosting market sentiment. Data shows that among the 31 analysts tracking Palantir, 20 have a “Buy” rating, 9 have a “Hold” rating, and 4 have a “Sell” rating. At the beginning of the year, only 9 analysts had a “Buy” rating. The consensus price target is around $190, implying about a 31% upside from Monday’s closing price.

The institutions that raised their ratings last month include UBS, Mizuho Securities, HSBC, Freedom Capital, Daiwa, Northland, Baird, and William Blair.

UBS analyst Carl Kilsted’s view is representative, stating in a February 26 report that Palantir is “the software industry’s top growth story, at the intersection of the two strongest spending trends—AI and data.” He added that the company’s valuation “has finally reached a level where many investors can make a strong case for its valuation.”

This view was confirmed in last month’s earnings report, where Palantir not only surpassed Wall Street expectations but also provided a much stronger-than-expected revenue forecast. Data shows that Palantir’s expected revenue growth over the next 12 months is 73%, ranking fifth among the S&P 500 companies.

All of this gives Palantir significant momentum during a period of geopolitical uncertainty. As investors focus on the duration of the war and its impact on the global economy, Palantir stands out as one of the few companies that can truly benefit in times of turmoil.

In fact, the conflict may generate more global demand for its products and services.

“Conflict helps Palantir acquire new customers, especially as tensions escalate in the Middle East,” said senior tech analyst Mandip Singh. “One of Palantir’s main applications is assessing supply chain risks in the commercial sector. Companies with exposure to the Middle East face huge supply chain risks and could become customers. While there has been geopolitical tension before, war brings a new sense of urgency.”