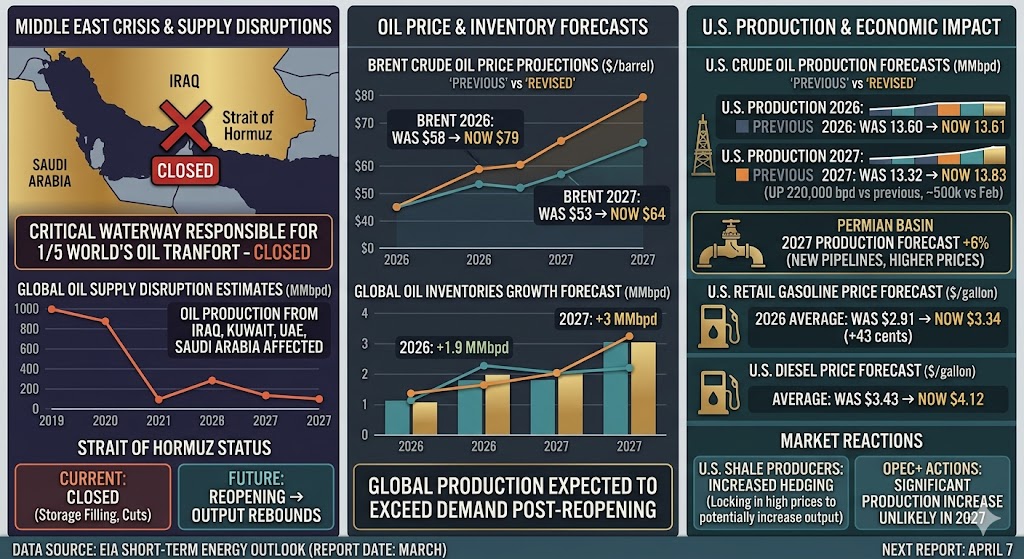

The U.S. Energy Information Administration (EIA) has raised its forecast for U.S. oil production next year, expecting an increase of 220,000 barrels per day to reach 13.83 million barrels per day. This comes amid soaring oil prices triggered by disruptions in supply from major oil-producing countries in the Middle East. The EIA has also raised its forecast for oil prices this year. Additionally, the EIA has revised its forecast for U.S. retail gasoline prices in 2026, expecting them to average $3.34 per gallon, 43 cents higher than the previous estimate. The EIA predicts that once the Strait of Hormuz resumes operations, global oil production will continue to exceed demand.

The recent surge in oil prices due to supply disruptions in the Middle East has led to the EIA’s upward revision of its U.S. oil production forecast. According to the EIA’s short-term energy outlook report released on Tuesday, U.S. crude oil production is expected to increase by 220,000 barrels per day to 13.83 million barrels per day in 2027, compared to the previous forecast of 13.32 million barrels per day. The EIA now expects production to be 13.61 million barrels per day in 2026, up from the previous forecast of 13.60 million barrels per day.

The EIA’s latest 2027 forecast has been raised by approximately 500,000 barrels per day compared to its February prediction. Earlier reports had indicated that U.S. oil production would peak this year and start to decline in 2027.

The EIA states in its latest report, “Since the impact of oil price changes on production takes time to materialize—from investment decisions, rig deployments, to the completion of wells and initial oil production—our forecast shows that the impact of rising oil prices will be more significant in 2027 than in 2026.”

At the end of last month, U.S. and Israeli strikes on Iran sparked widespread retaliation from Iran, effectively closing the critical Strait of Hormuz, a waterway responsible for transporting about one-fifth of the world’s oil. With storage capacities gradually filling up, oil production in the region has been affected by production cuts.

The EIA estimates that the oil production affected by the closure of the Strait of Hormuz will peak in early April, primarily from Iraq, while Kuwait, the UAE, and Saudi Arabia will see relatively smaller impacts.

The EIA report also notes that the prolonged closure of the Strait of Hormuz will lead to further declines in oil production from the Middle East in the coming weeks. Once the Strait of Hormuz reopens, the previously shut-in production will gradually be restored, and output will rebound. The EIA anticipates that once the Strait of Hormuz is fully operational, global oil production will continue to exceed consumption demand.

Given that significant inventory build-up is expected during the forecast period, the EIA predicts that OPEC+ will not significantly increase production next year. The EIA forecasts that global oil inventories will grow by 1.9 million barrels per day in 2026 and by 3 million barrels per day in 2027.

This week, U.S. oil prices briefly spiked to nearly $120 per barrel before retreating to around $84 per barrel. The EIA has once again raised its oil price forecast for this year. It now expects the price of Brent crude to average $79 per barrel in 2026 (up from the previous estimate of $58 per barrel) and $64 per barrel in 2027 (up from $53 per barrel).

Due to the Middle East conflict, the EIA expects Brent crude prices to remain above $95 per barrel for the next two months, drop to below $80 per barrel in the third quarter, and fall to around $70 per barrel by the end of the year.

This surge in oil prices has pushed U.S. retail gasoline prices to their highest levels since July 2024. The EIA has raised its forecast for 2026 U.S. retail gasoline prices to an average of $3.34 per gallon, 43 cents higher than the previous estimate.

The rise in oil prices has also triggered a wave of hedging activity among U.S. shale oil producers to lock in high prices for future sales. This move may enable producers to increase output even if oil prices fall in the coming months.

Additionally, the EIA has raised its forecast for crude oil production in the Permian Basin by 6% for 2027, citing new pipeline capacity and higher oil prices as key factors supporting growth in the region.

Moreover, since the outbreak of the Middle East conflict, global diesel prices have surged. The EIA expects U.S. diesel prices to continue rising, with the average price expected to increase from $3.43 per gallon in 2026 to $4.12 per gallon.

The EIA’s next short-term energy outlook report will be released on April 7.