On December 17, 2025, ABM Industries Incorporated (NYSE: ABM) released its Q4 2025 financial results, revealing a mixed picture of record quarterly revenue growth, a significant earnings miss relative to consensus expectations, and updated guidance for fiscal 2026 that drew a cautious market reaction. ABM stock price experienced volatility as investors parsed revenue strength against weaker profit performance and earnings guidance.

ABM Industries reported Q4 revenue of approximately $2.30 billion, reflecting a 5.4% year-over-year increase and record quarterly top-line performance, while reported EPS of $0.88 missed estimates of about $1.09. Despite the earnings shortfall, operating improvements and organic growth indicated improving business fundamentals. The company also reiterated its broader fiscal outlook with a projected earnings range for fiscal 2026, signaling management confidence in continued expansion.

This report offers a comprehensive examination of ABM’s latest financial results, interpret key trends in profitability and revenue growth, analyze strategic business initiatives and market positioning, and conclude with a reasoned outlook for ABM stock — including a buy, hold, or sell recommendation.

Company Overview: ABM Industries and Its Business Model

ABM Industries is a U.S.–based provider of integrated facility management and services, operating across multiple end markets including business and industry, aviation, education and technical solutions. Its services span workforce management, janitorial and cleaning services, energy solutions, parking and mobility, and specialized technical services. The firm’s diversified service portfolio aims to generate recurring revenue through long-term contracts with commercial, industrial, institutional, and governmental clients.

Given ABM’s service-intensive model, its earnings performance is affected by broad macroeconomic conditions (such as corporate capex and facility spending trends), cyclical labor costs, contract renewals, and demand fluctuations in key end markets like aviation. The company has historically delivered modest organic revenue growth with a focus on operational efficiency.

Latest Financial Results — Headline Numbers and Overview

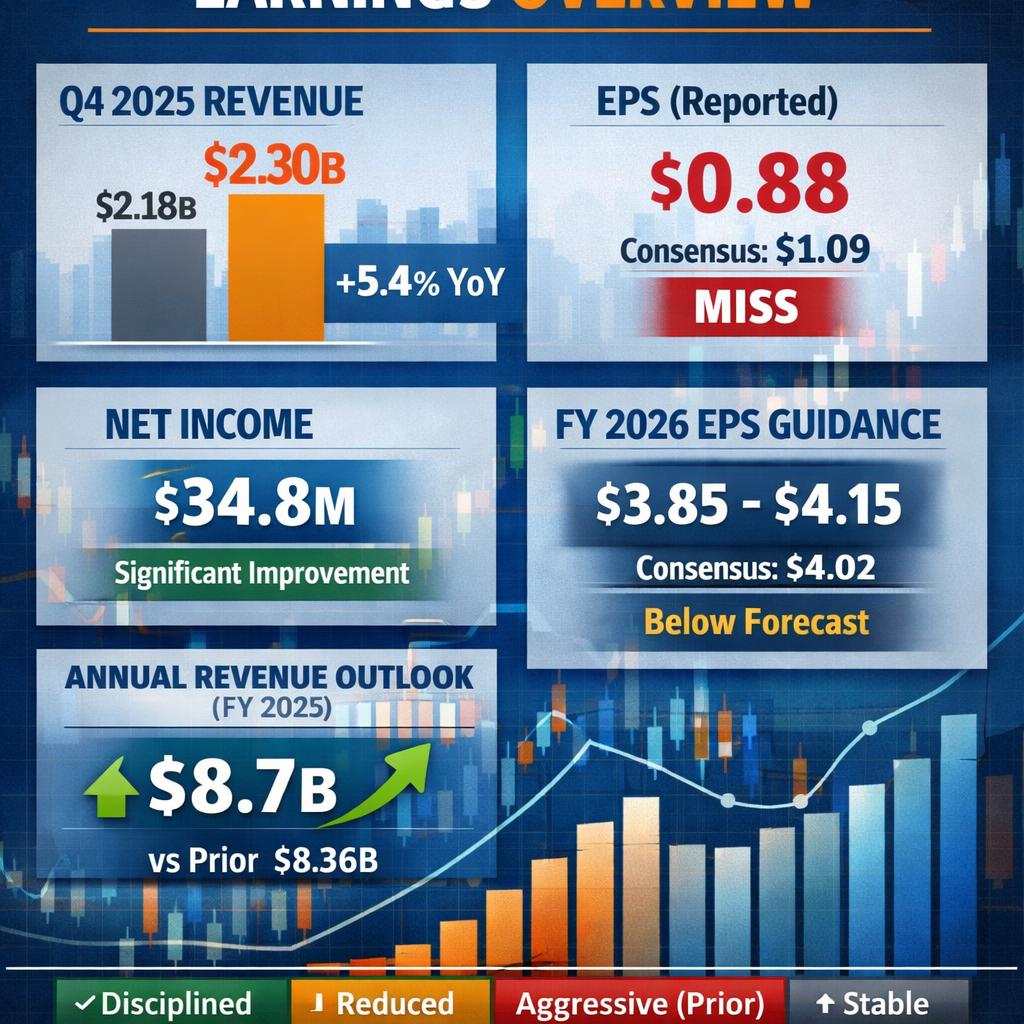

The table below summarizes ABM’s key financial results from its reported Q4 2025 earnings — as disclosed on December 17 — alongside comparable figures from the prior year and market expectations.

ABM Industries Q4 2025 Financial Highlights

| Metric | Q4 2025 Actual | Q4 2024 Year-Ago | Consensus Estimate | Remark |

|---|---|---|---|---|

| Revenue | ~$2.30 B | ~2.18 B | ~2.28 B | +5.4% YoY revenue beat MarketScreener+1 |

| EPS (Reported) | $0.88 | ~$0.90 | ~$1.09 | Missed consensus MarketScreener+1 |

| Net Income | ~$34.8 M | ~Net loss prior | Subdued | Significant improv. Investing.com |

| Organic Growth | 4.8% | (Comparable) | — | Continued expansion 雅虎财经 |

| Annual Revenue (FY2025) | ~$8.7 B | ~8.36 B | — | +~4.6% YoY chartmill.com |

| FY2026 EPS Guidance | $3.85–$4.15 | — | ~$4.02 | Slightly below cons. MarketScreener |

Even as revenue growth met or exceeded expectations, profitability lagged relative to consensus and prior EPS forecasts — underscoring cost pressures and operational dynamics in the business services sector.

Revenue Growth: Breaking Down Strengths and Sources

Record Quarterly Revenue with Thoughtful Organic Growth

ABM’s reported Q4 revenue of $2.30 billion represented a 5.4% year-over-year increase, marking the highest quarterly top line in the company’s history. Growth was attributable to both organic expansion (4.8%) and contributions from portfolio enhancements, including recent commercial wins and acquisitions.

Organic growth was balanced across several of ABM’s service segments:

- Technical Solutions: Growth was particularly strong due to increased demand in specialized services such as electrical, mechanical, and engineering maintenance projects. Segment contributors reported over 16% growth, reflecting deeper penetration in industrial accounts and microgrid solutions.

- Manufacturing & Distribution: Expanded client acquisitions in manufacturing settings bolstered this segment’s revenue.

- Aviation Services: New contract awards at airports supported segment growth and diversification.

The balanced nature of revenue expansion reflects resilience in ABM’s core markets and indicates that the business is becoming better insulated against localized demand downturns in any single end market.

Annual Revenue Trajectory and Durable End-Market Demand

For the full fiscal year 2025, ABM reported roughly $8.7 billion in revenue, a ~4.6% increase year-over-year. This steady annual growth demonstrates the company’s ability to sustain expansion despite headwinds in labor cost inflation and competitive pricing pressures.

These results suggest that ABM’s service offerings continue to resonate with enterprise customers seeking integrated facility management solutions, and that long-term contracts contribute meaningfully to revenue stability.

Profitability Analysis: Earnings, Margins, and Operational Levers

Earnings Per Share: A Miss Relative to Expectations

The reported EPS of $0.88 for Q4 2025 was below the consensus estimate of roughly $1.09, representing an earnings miss of around 19–20%. Several factors likely contributed to this shortfall:

- Cost pressures: Rising labor and materials costs, especially in high-touch service segments, weighed on margins.

- Pricing dynamics: Competitive pricing in certain markets may have limited pricing leverage.

- Acquisition and integration costs: Incremental investment spending related to strategic acquisitions could have diluted near-term earnings.

Nevertheless, it’s important to note that net income improved meaningfully versus the prior year, moving from a net loss to a positive $34.8 million in net income, a significant improvement in bottom-line dynamics.

Margins and Operational Efficiency

While revenue grew, ABM’s profitability profile reflects persistent operational cost challenges that are common in service-intensive businesses. Gross margins were constrained relative to the strong top-line performance, implying that cost control remains a priority area for management. The ability to improve margins will be a key determinant of earnings sustainability and future valuation.

Despite the shortfall in EPS relative to expectations, the improvement in net income from a prior loss indicates that ABM is advancing toward delivering profitable growth — a crucial validation of management’s operational improvement efforts.

Strategic Initiatives: How ABM Is Positioning for Future Growth

Targeted Service Expansion and Portfolio Optimization

ABM has undertaken several strategic initiatives designed to strengthen its competitive positioning:

- Acquisition of WGNSTAR: The acquisition aims to expand ABM’s technical capabilities in specialized services, including those overlapping with semiconductor and advanced manufacturing infrastructure support, potentially creating cross-selling opportunities.

- Focus on Higher-Value Segments: Growth in technical solutions, aviation services, and manufacturing support suggests a deliberate shift toward differentiated services that command stronger long-term revenue streams and deeper customer engagement.

- Contract Bookings and New Wins: ABM reported strong new bookings, with approximately $1.9 billion in new sales, indicating effective sales execution and healthy demand pipelines.

These strategic efforts are aimed at not only expanding ABM’s addressable market but also improving margins over the medium term through a greater mix of higher-value service offerings.

Operational Improvements and Efficiency Gains

Management indicated that a restructuring program is expected to yield approximately $35 million in annualized savings, with most savings anticipated to materialize in fiscal 2026.

This focus on cost optimization is important given the mixed EPS results. While top-line growth remains intact, improved profitability will be essential to converting revenue gains into sustainable shareholder value.

Market and Competitive Position

ABM operates in the broader facility management and integrated services sector, competing with both national peers and regional service providers. Its diversified service portfolio provides a degree of competitive advantage, especially in large enterprise accounts requiring a broad range of services under a single partner.

Relative to peers, ABM’s revenue growth rate is solid, though earnings margins and EPS performance suggest room for operational improvement. Industry metrics show that ABM’s valuation multiples remain moderate relative to broader service sector benchmarks, likely reflecting investor caution given recent earnings variability.

Investor Sentiment and Analyst Views on ABM Stock

Analyst coverage of ABM stock generally leans toward a Buy to Hold consensus, with 12-month price targets suggesting potential upside from current levels. Average price targets around $54 per share imply roughly 20–30% potential upside versus recent trading levels.

However, some models indicate a Hold consensus among certain platforms, reflective of the stock’s mixed near-term performance and earnings miss.

ABM Stock Price Review: Where the Market Stands

As of the latest data, ABM stock has experienced moderate volatility, with prices in the low-to-mid $40 range following the earnings release. According to recent pricing data:

- ABM stock price is trading around $42–$47 per share near mid-December 2025.

- The 52-week trading range shows a high near $54–$56 and a low near $40, illustrating significant trading breadth.

These fluctuations reflect investor reactions to earnings dynamics, cost pressure concerns, and overall economic conditions affecting service demand.

Detailed Financial Interpretation: Key Trend Drivers

To understand what lies beneath the headline revenue and earnings figures, it’s instructive to parse where growth is originating and how cost structures are evolving.

1. Organic Revenue Growth as a Foundation

ABM’s organic growth (4.8%) suggests that core demand for facility services remains healthy. This is particularly notable in light of macroeconomic headwinds that can weigh on corporate discretionary spending. The fact that ABM’s organic growth outpaced overall sector growth rates indicates solid competitive positioning.

2. Segment-Level Drivers: Technical Solutions and Aviation Momentum

Segments such as technical solutions and aviation not only contributed disproportionately to revenue growth but also signal structural shifts in ABM’s business mix. High-technical content services often have higher pricing leverage and longer contract durations, which bode well for revenue stability and margin potential over time.

3. Profit Mix Versus Cost Base Dynamics

Despite healthy top-line growth, the EPS miss underscores lingering cost pressures and margin compression in certain segments. Labor costs, subcontractor expenses, and competitive pricing in janitorial and basic services can constrain profitability. Management’s focus on efficiency programs and restructuring is designed to address these dynamics, but full impact may not be realized immediately.

Overall, the Q4 results represent a transition point, where revenue growth is emerging from diversified sources, but earnings resilience remains a work in progress.

Risks and Uncertainties

Investors should remain mindful of several risks inherent to ABM’s business model and broader market conditions:

- Labor market costs: Persistent wage inflation can squeeze margins.

- Contract renewal risk: Long-term client contracts can sometimes be renegotiated at lower rates, particularly in challenging economic environments.

- Competition: Both national and regional competitors may exert pricing pressure.

- Economic cycles: Facility services demand can correlate with broader economic activity, especially in sectors like aviation and commercial real estate.

These factors suggest that while revenue growth is promising, investors should carefully benchmark earnings trajectory against cost performance over time.

Outlook: How the FY2026 Guidance Shapes Expectations

ABM’s fiscal 2026 earnings guidance — projecting adjusted EPS in the range of $3.85 to $4.15 — is slightly below consensus estimates, indicating management’s cautious view of near-term profitability even amid revenue growth.

This guidance reveals that ABM expects continued revenue expansion but acknowledges margin pressures and strategic spending related to restructuring and acquisitions. The company’s ability to improve operating efficiency and extract synergies from recent strategic investments will be central to beating this guidance.

Investment Thesis: Buy, Hold, or Sell?

Bullish Considerations

- Record revenue and solid organic growth: ABM is growing its core business even in competitive markets.

- Strategic expansion into higher-value services: Technical solutions and aviation segments provide differentiated revenue streams.

- Improving net income: Turnaround from prior net losses underscores operational improvement.

Bearish Considerations

- Profitability challenges: The earnings miss and cost pressures temper enthusiasm.

- Modest earnings guidance: Fiscal 2026 outlook implies caution rather than acceleration.

- Market valuation weighs risk: Current multiples reflect guarded investor sentiment.

Investment Recommendation

Hold with selective accumulation on weakness. ABM stock appears positioned for moderate long-term appreciation based on diversified revenue growth and solid service demand, but near-term earnings headwinds and margin pressures suggest the stock may underperform more aggressive growth peers. Investors seeking income and stable, growing revenues may consider a measured allocation, while more aggressive growth-oriented investors may prefer to remain on the sidelines until margin improvement becomes more evident.

Conclusion

The December 17, 2025 ABM Financial Report painted a nuanced picture: record revenue growth and improved operational performance juxtaposed with an earnings shortfall and muted profitability expansion. This blend of strengths and weaknesses explains the cautious investor response in the ABM stock price.

ABM Industries is navigating a transition toward higher-value service offerings and broader market penetration. Its strategic initiatives — including acquisitions, segment expansions, and operational restructurings — are positioning the business for long-term resilience. However, margin pressures and macroeconomic uncertainties necessitate a disciplined investment approach.

For long-term investors who emphasize stable, contract-driven revenue streams and diversified service exposure, ABM may offer potential value accumulation over time. Nonetheless, expectations for strong near-term earnings acceleration should be tempered.